This article was written by Matt Green, Partner and Head of Blockchain and Digital Assets, and was published on Thomson Reuters Regulatory Intelligence on 28 April, 2026. Subscription may be required to view.

You can read the full article as published on Thomson Reuters below.

This article details the recovery of Monero (XMR), a notoriously difficult-to-trace privacy coin, following a fraud. The Monero was ultimately recovered through coordinated legal, investigative and law enforcement action.

The author’s client received a call from an individual purporting to represent a cryptocurrency exchange. During the call, the fraudster asserted that the client’s exchange account had been compromised and urgently instructed the client to transfer assets to a trust wallet as a protective measure.

The fraudsters were in possession of the client’s personal and account details, likely obtained via data breaches. This gave the scam credibility and induced the client to act quickly.

As a result, the client transferred significant holdings of bitcoin and ether to the fraudster. These were subsequently routed through a series of exchanges and converted into other digital assets, including Monero.

Tracing, initial exchange engagement

A forensic blockchain investigation traced asset movements to the exchanges FixedFloat, HitBTC and ChangeNOW, where the bitcoin and ether had been converted into other currencies.

Letters were urgently sent to those exchanges to confirm receipt of the criminal proceeds and to provide instructions on what to do next. The responses varied: some exchanges failed to respond, while others confirmed that certain funds had already been dissipated.

Importantly, some of the assets had been converted into Monero and remained identifiable at ChangeNOW, which then froze what it had and confirmed compliance with the requests made in the letters.

Law enforcement involvement, freezing order

With assistance from the Metropolitan Police cryptocurrency investigations team, and relying on blockchain forensics, an application was made to Westminster Magistrates’ Court for a crypto wallet freezing order.

The court granted a freezing order under section 303Z37(2) of the Proceeds of Crime Act 2002, formally freezing the Monero held at ChangeNOW for an initial period of six months. This step was critical in preserving the remaining assets while further recovery steps were pursued.

Order to release cryptoassets

Upon expiry of the six-month freezing period, an application was made for a declaration that the Monero belonged and was deliverable to the clients.

The Court granted a cryptoasset release order for Monero assets pursuant to sections 303Z50(4) and (5), and 303Z51(4) and (5) of the Proceeds of Crime Act 2002. Service of the order on ChangeNOW was effected by the Metropolitan Police.

Custody, attribution and transfer

Given the technical complexity of sending Monero, which is designed to evade tracing, specialist asset custody and attribution support was required.

Asset Reality, which seizes, manages and disposes of traditional and digital assets, was instructed to receive, attribute and manage the Monero. To mitigate attribution risk, an initial test transfer was conducted. Asset Reality required specialist knowledge to identify which Monero assets were sent by ChangeNOW, which is highly uncommon. The remaining balance was subsequently transferred once verification was complete.

Outcome

Once the Monero was in Asset Reality’s custody, it was able to locate an approved buyer for onward handling and sale. The client then received fiat currency into his personal account. This marked the successful recovery phase of assets that had initially appeared, by design, almost impossible to recover.

Legal, practical takeaways

This matter illustrates several important points for practitioners and victims of cryptoasset fraud:

Recoveries remain possible, even where assets are converted into privacy coins.

The use of Monero or a similar, privacy-focused cryptocurrency does not render recovery efforts futile when timely tracing, freezing and expert handling are deployed.

Law enforcement engagement is increasingly effective and proactive.

The involvement of specialist police crypto teams can be decisive, particularly in securing freezing and release orders under the Proceeds of Crime Act 2002.

This case demonstrates the practical effectiveness of combining civil recovery mechanisms under the Proceeds of Crime Act 2002 with technical blockchain expertise and law enforcement support. It provides a clear example that even in cases involving Monero, the legal system has viable tools to preserve and recover misappropriated cryptoassets when action is taken promptly and collaboratively.

What “crypto‑funded” property purchases usually mean in practice

Although UK property can be acquired with crypto assets in some circumstances, most purchases that are described as “crypto‑funded” are completed in sterling. In practice, buyers typically sell digital assets for sterling using an exchange or broker and then send the monies to their solicitor who pay the deposit and completion monies following an otherwise standard conveyancing process.

This liquidation matters as the process requires the buyer’s side to conduct enhanced KYC, and AML “source” checks prior to the purchase timetable. In essence, the seller’s experience often looks completely ordinary (they receive the agreed purchase price in sterling through the usual channels).

A six-step process to buying property using the proceeds of selling your crypto

Step 1: Convert your crypto into sterling

Most property buyers convert their crypto into sterling via an exchange; for larger amounts, conversions are often staged (e.g., in tranches) to manage volatility, pricing, and execution slippage. Some also use over-the-counter brokers for larger or more controlled conversions.

Practical tip: The conversion stage is frequently where timing pressure starts, because market moves can affect the sterling amount available for deposit/completion.

Step 2 – Transfer the funds to a bank account

Even as banks have become more familiar with crypto over time, not all are equally comfortable receiving substantial funds from crypto exchanges. Larger transfers can trigger queries about the origin of funds as part of standard AML/KYC procedures.

If you are buying with a mortgage, consumer-facing mortgage guidance indicates lenders may accept the proceeds from crypto sales, but often with extensive documentation requirements – and in some cases a preference that funds have been held in a bank account for a period (known as “seasoning”) before being treated as deposit-eligible.

Step 3: The real gating factor: your solicitor’s Source of Funds (and sometimes Source of Wealth) sign‑off

For many buyers, the decisive issue is not whether the property can be bought with crypto-derived wealth, but whether the buyer can find a solicitor able to address the enhanced Source of Funds (and, where relevant, Source of Wealth) requirements in time to complete the purchase within the required timeframe. A solicitor cannot proceed unless they are comfortable the source of funds is legitimate and properly evidenced.

Where wealth originated in crypto, delays often arise even when the funds are entirely legitimate, because often advisors do not have the expertise to interpret blockchain ledgers, reconcile exchange statements, or make sense of different “crypto wealth” pathways (e.g., long‑term holding, trading activity, and other ecosystem events that crystallise value).

Practical takeaway: Treat Source-of-Funds work like a mission‑critical workstream. If it begins late, it can become the single point that determines whether you complete on time.

Step 4: Build a clean evidence pack (so queries do not derail exchange/completion)

To reduce any potential friction, compile a clear “audit trail” showing the pathway from the fiat source of wealth (like an inheritance, or salary) to the purchase of crypto assets, and from where those assets are held, traded or swapped, to those funds being liquidated into sterling and deposited into your bank account. Common components include:

“real world” source of wealth documents, like bank statements, completion documents from the sale of a property or documents evidencing money from an estate or trust,

exchange or broker statements confirming liquidation/conversion,

bank statements showing receipt of the sterling proceeds, and

supporting records linking holdings to liquidation (wallet evidence / transaction histories where relevant).

A short, written narrative (“how the assets were acquired, where they were held, and how/when they were sold”) can help your solicitor and bank interpret the documents quickly and reduce repeated follow‑ups.

Step 5: Address tax early (because conversions can trigger liabilities)

In the England and Wales, converting crypto into fiat currency, and even exchanging one crypto asset for another, can trigger a tax position depending on the nature of the activity and your circumstances. Leaving tax and records until late in the process can create avoidable delay close to completion.

Practical tip: Crypto friendly apps like Koinly can assist with tax and accounting affairs and are valuable to help evidence the flow of funds.

Step 6 – Completion

Once funds are held in sterling and your solicitor is satisfied on source checks, exchange and completion can proceed in the usual way: funds are transferred, formalities are completed, and registration steps follow normal conveyancing practice.

Case study: an auction purchase under a strict “notice to complete” timetable

Below is a real‑world style example (with identifying detail removed) showing how Source‑of‑Funds issues can become existential when the purchase timetable is compressed.

The situation

An individual successfully secured a commercial property at auction intending to fund the purchase using liquidated cryptocurrency investments. A standard auction deposit (10%) was paid.

The problem

His usual solicitors refused to act as they could not fulfil the enhanced due diligence requirements needed to verify the crypto-derived funds to the standard required for a property transaction. Having failed to complete on the contractual completion date and with the final deadline looming, the buyer faced substantial losses: loss of the deposit, loss of the asset, and potential wider reputational and financial consequences associated with a failed completion.

What was done

Lawrence Stephens was instructed with three days left of the Notice to Complete period remaining. A specialist team was instructed to produce a structured Source of Funds report designed to meet conveyancing compliance expectations. The work focused on making the crypto-to-sterling pathway legible and verifiable, including:

reconstructing early “on‑ramp” funding (how fiat currency entered the crypto ecosystem),

substantiating wallet control and mapping transaction flows, and

reconciling exchange records with liquidation history to show how proceeds became banked sterling.

The outcome

With the provenance work documented to a standard that satisfied compliance expectations, the conveyancing process was re‑stabilised and the transaction proceeded to completion within the deadline securing the investment for our client

Why this matters

This example illustrates a key reality of crypto‑funded purchases: the primary obstacle is often not the money itself, but whether professionals involved have the capability to evidence provenance convincingly and quickly – especially where the timetable (as in auctions) does not tolerate delays.

Lawrence Stephens are experts in this area.

Quick checklist to reduce the risk of delay (especially for auctions)

Before you bid / make an offer

Start your evidence pack early (exchange statements, wallet records, transaction history exports).

Prepare a one‑page “funds narrative” explaining acquisition, holding, liquidation and bank receipts.

If mortgage finance is involved, speak to a broker early about crypto‑derived deposits and whether “seasoning” expectations apply in practice.

During the off‑ramp (selling crypto for sterling)

For larger sums, consider staged conversions to manage execution and keep records clean.

Keep all trade confirmations and transfer receipts in one place to respond fast to questions.

In the run‑up to completion

Treat “Source of Funds” queries as urgent and respond with structured documentation quickly; late responses often become the critical path.

Why expectations will likely become more formal over time (UK context)

The UK is moving toward a comprehensive crypto regulatory framework that brings more crypto asset activities within the FCA perimeter, with the full regime expected to commence in October 2027.

HM Treasury has positioned these reforms as supporting innovation while improving standards around transparency, consumer protection, and resilience—factors that typically increase the formality of documentation and compliance processes across the ecosystem.

Conclusion

For most buyers, “buying property with crypto” in the UK usually means selling crypto for sterling and completing a standard sterling transaction. The true difficulty is often proving the pathway from digital assets to banked funds to the satisfaction of solicitors (and lenders where relevant) and doing so within the transaction timetable.

The auction case study shows how quickly this can become existential when deadlines are tight – and why early preparation and specialist capability can be the difference between completing and forfeiting a deposit

Important: This article is for general information only and does not constitute legal, tax, or financial advice. Crypto transactions and property purchases can create tax and compliance obligations, please ensure that you seek professional advice for your particular circumstances.

If you would like to discuss anything with a member of the Lawrence Stephens team, please contact cryptorealestate@lawstep.co.uk.

You can read the full article as published on Thomson Reuters below.

As traditional finance houses seek to diversify and enter the decentralised world (bitcoin’s value increased by 132% over the last five years), the obvious risks are less technical and more human.

Senior boards are hiring staff whose job specifications are sometimes not fully understood or wildly unfamiliar. Crypto traders often possess specific knowledge that is not widely shared across an organisation, posing a significant risk to business operations.

Little exemplifies this pattern more than a recent UK High Court case (held in private) brought by a London hedge fund that found more than 1.9 million USDC (a stablecoin called Circle, whose value is pegged to the U.S. dollar) drained from their trading account. They had no idea how this happened, no clear leads and no technical vulnerabilities.

This article deals with how lawyers, investigators and blockchain forensic firms helped recover most of the funds within nine working days from being instructed through to recovery, and how the most “nuclear” of legal tools can be used to secure fast and substantial results.

Tracing stablecoins and the smoking gun

The approximately 1.9 million USDC drained was traced by Token Recovery, a blockchain forensics firm that confirmed the funds were consolidated into a single address and remained there for several days. From experience, in the event of a theft, funds are quickly laundered via tumblers and put out of reach by a process known as “smurfing,” whereby large sums of money are broken down into smaller transactions to remain undetected by anti-money laundering protocols and to frustrate tracing. The fact that this money remained in one place for several days indicated that the threat actor was likely unsophisticated and opportunistic.

It was suggested that the hedge fund conduct an internal investigation to determine whether any suspicious staff or activity indicated that the theft was an inside job.

The hedge fund found that one employee, a software engineer (“Mark”), had recently resigned, and according to access logs, took a particular interest in the targeted wallets on the day of the theft.

In response to certain behaviours during employment, the hedge fund had implemented human-resources-led monitoring software on his profile, which took a screenshot of his computer every few seconds, creating a video of his activities. The software had largely been forgotten, but was now vital evidence, given the direction of blockchain forensics.

The video showed that Mark:

Reviewed the balances of the hedge fund’s crypto trading accounts.

Logged into the relevant servers which ran the trading engines.

Initiated memory dumps of those engines and copied them to his local system.

Loaded the files into a debugger and immediately navigated to the relevant private keys, which gave any holder the ability to withdraw funds from the relevant account.

Then, moments later, searched Google for “Metamask” (cryptocurrency wallet management software) and “what is a Polygon wallet,” suggesting he intended to trade the funds on the Polygon market.

In all, this was key evidence, given there was no genuine reason for Mark to navigate to the private keys. It may have taken longer to consider this evidence without the forensics and laundering patterns.

Law enforcement

The incident was reported to police on several occasions, and a crime reference number was provided, to be handled by Action Fraud, a triaging service for law enforcement.

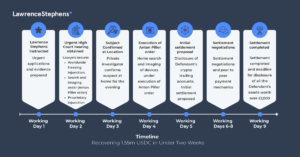

From the pace and manner following reporting, the hedge fund instructed its lawyers, law firm Lawrence Stephens Limited, of which the author is a partner, to make a move more quickly, given the evidence at hand. This is the timeline’s first working day.

Urgent injunctions, nuclear options

On the second working day, the hedge fund and its legal team appeared in the High Court on an urgent basis, seeking highly intrusive court orders.

The first was a proprietary injunction (an order to do or not do something with specific property or its traceable proceeds) over the approximately 1.9 million USDC, which in the meantime had started moving and was being laundered more professionally.

The second was a worldwide freezing injunction over Mark’s assets over £1,000 in value and up to $1.9 million (approximately £1.5 million) in total, preventing him from moving assets or money, except for his capped living expenses, without being in contempt of court.

The third was a search and imaging order (also known as an “Anton Piller”[1] order), which allowed the legal team to search Mark’s premises for relevant documents and electronic devices, gain access to relevant accounts, compel the delivery of information and hardware and image the contents of those devices.

This would ensure that critical evidence could be searched for, seized, recorded and preserved for future use. In short, it prevented Mark from destroying evidence that could potentially prove his liability and reveal to the hedge fund what happened to its stolen USDC.

Anton Piller orders are rare, granted by the courts in limited circumstances and widely viewed as the civil court’s “nuclear option.”There must be an extremely strong prima facie case to persuade the court to make such an order, and the court appoints a supervising solicitor to safeguard a defendant’s interests during the search.

The hearing was on an “ex parte” (without notice) basis, meaning Mark had no knowledge that this was happening. The court issued the orders that night. A private investigator was then hired to follow Mark’s movements and monitor his home.

Working day three was spent preparing documents for service and instructing forensic imaging experts (JS Held) who would image devices, and the supervising solicitors.

Home entry

Execution of the search was planned for working day four, a Friday. Service of documents was limited to between 0930 and 1400. There was always a risk that Mark might not be at home, that he (or any cohabitant) might refuse to open the door, or that he might jump out of the window and run away. In any of those cases, a new court order would likely be required. Had he wilfully refused to open the door, he would have been in contempt of court.

The investigator confirmed that Mark was seen entering the house the night before, and there was no evidence that he had left. The supervising solicitors knocked just after 0930 and woke the house. A relative opened the front door, shortly followed by Mark, who thought it was an Amazon delivery.

Mark was immediately served with the Anton Piller order. He had two hours to seek legal advice before the search party entered and was immediately required to hand over his mobile phone and other relevant electronic devices. He was not to be left out of sight for the day.

Search party

Two hours later, the legal team search party was allowed in. There was no protestation or outward denial of wrongdoing, and Mark granted access to the search party. The incumbents’ movements were monitored carefully to mitigate the risk of Mark destroying key documents or dissipating his assets. As the funds are digital, any internet access is high-risk, and 30 seconds locked in a toilet is enough time to put the USDC or other assets out of reach. As ordered by the judge, his phone was imaged on site and returned without delay.

All relevant electronic items were secured, including mobile phones, a PlayStation5, USB sticks, memory cards and a gaming computer. Physical reviews of paper, including receipts and pages of old cheque books, might reveal seed phrases (a collection of innocuous words, which, when input, give access to a crypto wallet) or private keys.

Mark was required to give the forensic imaging team access to all relevant accounts, including financial and crypto trading accounts. He maintained various cryptocurrency accounts with several providers and also held an account for Monero, a privacy-focused cryptocurrency designed to make tracing difficult.

The search lasted until around 1730, a time deemed reasonable to avoid unnecessary intrusion. The next two days were a weekend.

Freezing order

Mark was also served with the worldwide freezing and proprietary orders on the search day. Although he could technically move funds and dissipate assets, if it were found that he had done so after service, he would have been in contempt of court (a criminal offence). The power of that deterrent may have been reinforced by his mother, who happened to be a lawyer. Non-compliance, in his mind, may be outweighed by the value of the assets.

The freezing order also required him to detail all worldwide assets worth more than £1,000 on working day nine. This is vital. If he had the stolen funds or any proceeds, he must disclose them — unless, in limited circumstances, they are incriminating — or face contempt of court.

Settlement negotiations

Settlement offers yield quick results, especially when court hearings are imminent and pressure is greatest. As the first hearing was ex parte, the process required a further hearing two weeks later to allow Mark, the respondent, to seek to amend, discharge or agree to continue the orders. This is called a “return date” and is for the benefit of the respondent following ex parte hearings.

Mark’s lawyers made various attempts to settle. However, on working day nine, no agreement had been reached, and Mark was required to disclose his assets by 1730.

This was the overwhelming pressure point for settlement, because without a deal, Mark would now have to disclose his assets.

Eventually, Mark offered to agree to stay proceedings and discharge the orders, after which he would send more than 1.5 million USDC to the hedge fund directly, on a peer-to-peer basis.

Since trust was low, the preferred mechanism was inverse, such that the parties would agree that, upon receipt of Mark’s funds, the hedge fund’s lawyers irrevocably undertook to file a consent order (agreed by the parties) to stay proceedings and discharge the orders, subject to a short contract detailing terms. Mark was to send the funds in two stages, one dollar first, then the balance, to ensure transaction integrity.

The hedge fund made a take-it-or-leave-it offer: recover the money first, or Mark discloses and the parties proceed to litigation, knowing he had more than 1.5 million USDC that could be paid into the court as security during the proceedings. Mark took the deal.

Peer-to-peer settlement

This was a pure peer-to-peer settlement. The respective lawyers did not hold nor were they in any way in control of the flow of funds. On a call, Mark sent the first dollar, which the hedge fund received. Notably, the sending address was now identifiable, given that the transaction took place, and the hedge fund conducted a cursory review of the address.

Mark then paid the balance directly to the hedge fund.

Upon receipt, the consent order was filed, and proceedings were stayed. This was working day nine.

Decisive action

Understanding blockchain analytics helped to identify Mark, where there were no other obvious targets in the aftermath of an emergency. Convincing evidence of wrongdoing led to draconian injunctions and the Anton Piller order, which put enormous pressure on Mark. The settlement offer resulted in Mark’s disclosure of approximately 1.5 million USDC, which was the determining factor.

Within nine business days, the hedge fund’s team had changed the position from a complete unknown to obtaining more than 80% of the value of lost USDC, the hedge fund being satisfied that the balance had been dissipated and/or not worth the cost to pursue.

Often, published court proceedings involving lost cryptocurrency have yielded less-than-satisfactory results for victims. Accordingly, it is important to share success stories and show that recovery is real when the facts align and the analytics are well understood.

[1] Anton Piller KG v Manufacturing Processes Ltd [1976] Ch. 55

Matt Green, Head of the Blockchain and Digital Assets sector at Lawrence Stephens and Chair of the techUK Digital Assets Group, has been instrumental in developing their “2030 Vision- A roadmap for Building a Digital Assets Economy”, which launched on 16 October.

Designed to share insights on current and anticipated use of distributed ledger technologies, the Vision 2030 draws on perspectives from across the Blockchain and Digital Assets ecosystem – from across Layer-1 chains, professional advisors, to financial houses, blockchain forensic software providers and beyond – identifying the opportunities that will help strengthen UK’s position as a global financial hub, a centre of innovation and a market where technology is used for good.

In recent years, regulators, policymakers, and governments have each mapped their digital ambitions. The UK Digital Strategy 2017 highlighted the economic benefits of digital skills, while the 2022 update focused on establishing the UK as a leading technology hub. More recently, the UK International Development’s Digital Development Strategy 2024–2030 signalled a broader digital transformation of society. This was reinforced in the Chancellor’s Mansion House speech earlier this year, which committed to “drive forward developments in blockchain technology… so that UK financial services can be at the forefront of digital asset innovation.”

The 2030 Vision brings together industry views on where we are today, where we are heading, and what is needed to ensure that by 2030 the UK is not just adapting to change – but leading it.

Matt Green, Director and Head of Blockchain and Digital Assets, is a regular commentator on all things crypto and recently featured in BBC’s File on 4, one of the UK’s most respected investigative journalism programmes.

File on 4 has built a reputation for in-depth investigative reporting on some of the most pressing topics in society, from political scandals and corporate misconduct to human rights and financial crime. Produced by BBC Radio 4, the programme is known for shaping public understanding and policy on the UK’s most complex issues and has a weekly audience running into millions.

In this episode, which aired on the 30 September, File on 4 investigated the surge in phone thefts across London and the associated theft of funds from online accounts. In 2024 alone, there were up to 80,000 devices stolen in London’s streets and transport network. The loss to users goes far beyond having to replace stolen devices, as gangs are now exploiting unlocked phones to access victims’ online banking and cryptocurrency accounts.

Matt offered his expert insight into why crypto assets are particularly attractive to criminals, and how victims’ funds are emptied and transferred into criminal accounts: “The problem is that there are no regulatory provisions that ensure you can get your money back. You have to spend, as a consumer, a good deal of money paying for investigators and lawyers to seek to recover your funds. That is expensive, it doesn’t always work because funds can be sent to various jurisdictions which don’t always comply with court orders, and it makes the process a lot more difficult. I would like it so that there is some sort of duty or obligation for crypto currency exchanges to play a role in helping consumers and protect them further.”

Known for his work tracing and recovering crypto assets across borders, Matt regularly advises on high-value disputes involving blockchain technology and has helped shape UK legal precedent on digital property. As part of his role as chair of techUK’s Digital Asset Working Group, he is closely involved in the drive to improve regulation to help consumers recover stolen digital assets.

You can listen to the full podcast here, Matt enters the conversation at 29m16s.

To read more about our blockchain, digital and crypto assets services, please click here.

Director and Head of Blockchain and Digital Assets, Matt Green, has co-signed a letter to the UK Government alongside a coalition of leading associations from the digital, finance, and technology sectors, proudly representing techUK.

The letter, addressed to the Secretary of State for Business and Trade, urges that distributed ledger technology (DLT) – particularly tokenisation and stablecoins – be included as a core strand of the upcoming UK-US Tech Bridge. The signatories highlight that this transatlantic initiative presents a once-in-a-generation opportunity for the UK and US to set global standards in digital finance, strengthen their markets, and reinforce their joint leadership in financial innovation.

Matt Green, who signed in his capacity as Chair of the Blockchain Working Group at techUK, joined representatives from the City of London Corporation, UK Finance, Global Digital Finance, TheCityUK, the Crypto Council for Innovation, The Payments Association, and others in calling for the Government to seize this critical opportunity. The coalition’s effort was coordinated by the UK Cryptoasset Business Council.

Director Dominic Holden explores how businesses can protect themselves and mitigate the risks of a cyberattack, following the recent incident at Jaguar Land Rover, in Computer Weekly.

Dominic’s article was published in Computer Weekly, 9 September 2025, and can be found here.

A cyber-attack at Jaguar Land Rover has halted production lines and caused wide-spread disruption. How can businesses protect themselves and mitigate the risks of an attack?

A single cyber incident can halt production lines, dent customer confidence and wipe millions off a company’s share price – as Jaguar Land Rover (JLR) discovered after it was forced to shut down operations last week.

This incident is a stark reminder that cyber attacks are no longer rare, nor confined to small or poorly protected businesses, and that even global brands with sophisticated IT systems can be brought to a standstill. For UK businesses, the question is no longer if a cyber attack will happen, but when.

There is, though, much a business can do to prepare for a cyber attack to both reduce the prospect of falling victim to an attack and to mitigate the loss they can cause.

Preparation: A non-negotiable first step

Effective cyber resilience begins long before an attack occurs, and preparation can be key in mitigating the financial, technical or reputational damage. As such, many boards are now beginning to treat cyber security as a strategic priority, not a technical afterthought.

Effective preparation can encompass several aspects, and this can differ from business to business.

Often, this includes the creation of a clear, rehearsed incident response plan that identifies who does what in the first 72 hours and beyond, from isolating systems to briefing the regulator. The most effective plans are rehearsed by running crisis exercises and simulations so that staff know their roles, and leadership can practise decision-making under pressure.

Backing up your systems and testing that these systems can be restored quickly if compromised is also critical, with the JLR incident showing just how much damage a full shutdown of operations can cause.

Staff can also be more effectively trained to spot phishing attempts, unusual device activity and other red flags which may indicate an attempted breach of a company’s systems. Staff should also be made aware of the importance of ensuring that they install the updates that are rolled out by their IT team.

Cyber insurance is also key. There are many specialist brokers that can assist in tailoring a policy to the risks faced by the company. The process of obtaining the insurance often highlights issues with the company’s existing security and should provide essential support in the event of an attack.

Without such planning and preparation, a business will become more vulnerable to an attack and struggle to respond effectively when the pressure begins to increase.

The first 72 hours

If, despite your preparations, you fall victim to an attack, the first 72 hours are critical. This is where your planning pays off.

Where personal data may be at risk, the Information Commissioner’s Office (ICO) will need to be informed within 72 hours, and you may also need to notify your customers and suppliers of the risk. A PR team with expertise in crisis communications can be an important ally to avoid lasting reputational damage to the business.

Engaging law enforcement at the earliest opportunity is also advised. Reporting the incident to the police and Action Fraud creates a record that can support recovery and wider investigations. Notifying your insurers as soon as possible so you get support from specialist “breach response” advisers, including lawyers and computer forensic specialists, can avoid a misstep during a chaotic and stressful time.

A computer forensics team can move quickly to quarantine the affected systems and help you recover operations quickly, while also preserving evidence. A breach response lawyer will ensure you comply with your regulatory obligations and assist you in formulating a strategy to minimise the claims from suppliers and customers that can often follow.

The ransom question

One of the hardest decisions for businesses that fall victim to a ransomware attack is whether to pay a ransom – where one is demanded. While the National Crime Agency strongly advises against this, as there is no guarantee of restoration and payment encourages further crime, many organisations faced with operational paralysis may consider it a last resort.

Such ransom payments are often demanded in cryptocurrency, and their payment can be covered by insurance, so it is important for businesses to check their policies to see whether this forms part of their cover. It may also be possible to recover the ransom even after it has been paid. Specialist lawyers in crypto recovery can advise whether this is a possibility.

Lessons from JLR

The lesson from the JLR incident is simple: cyber security is no longer just an IT problem – it is a boardroom issue.

Boards must demand robust planning, allocate resources and ensure rehearsals are carried out. Only then can a business minimise financial and reputational damage when an attack occurs.

In April 2025, HM’s Treasury published a long-awaited overhaul of crypto regulation, via a draft statutory instrument to bring certain cryptoassets into our financial services regime – The Financial Services and Markets Act 2000 (Regulated Activities and Miscellaneous Provisions) (Cryptoassets) Order 2025.

In theory, this gives the UK an opportunity to now compete with other financial hubs by clarifying the rules on issuing cryptoassets. Other players have already taken the leap, notably in the European Union, Middle East and United States. For the UK, there is plenty of work needed to close this gap.

Head of Blockchain and Digital Assets Matt Green and BCB Group CEO Oliver Tonkin analyse HM Treasury’s overhaul of the UK crypto regime, and discuss whether this is too little too late in driving investment and innovation to the sector.

Matt and Oliver’s article was published in Thomson Reuters Regulatory Intelligence, 24 July 2025, and can be found here.

For more information on our blockchain, digital and cryptoassets services, please click here.

Following the Law Commission’s proposals for crypto and digital asset reform regime, Director Matt Green explores what these proposals mean for advisers – as well as those looking to recover stolen or hacked cryptocurrency.

Matt’s article was co-authored with Ashley Fairbrother, Partner at Edmonds Marshall McMahon.

Matt and Ashley’s article was published in FT Adviser, 16 July 2025, and can be found here.

In June 2025, the UK’s Law Commission proposed new powers to drastically help victims of fraud following the loss of cryptoassets where key details, like the bad actors’ details, are unknown. These proposals would allow courts to grant free-standing information orders at the outset of crypto fraud investigations, before the victim needs to commit to pursuing a substantive claim.

This may prove to be a vital legal reform and significantly increase access to justice, especially when victims have lost significant funds, and do not want to risk spending more money pursuing unknown parties who may or may not still hold funds.

The crypto fraud epidemic

Fraud concerning cryptoassets is a significant issue for consumers and businesses alike. Chainalysis’s “The 2025 Crypto Crime Report” notes that ‘pig butchering’ scams (i.e. scams via social engineering) have increased 40% year on year, and cost victims a total of $9.9 billion as of 2024. Separately, Chainalysis’s report notes that $2.2billion was stolen from crypto platforms across this period.

Last year, Action Fraud – the UK’s reporting centre for fraud and cybercrime – reported over 649,000 instances of investment fraud, with 66% attributed to crypto investment related schemes. Individuals are losing life savings, family homes and pensions, and taking out astronomical loans to pay fraudsters who demand more money to release funds already taken under the guise of investment profits.

Scams are often initiated by telephone calls, texts and emails from actors purporting to be from major cryptocurrency exchanges or banks who hold convincing personal data, usually obtained via data scraping, to harbour a victim’s trust and eventually extract funds. Assets are then typically laundered to facilitate human trafficking, drugs trades and organised crime.

Currently, victims can follow their funds across their respective blockchains by providing practitioners with their transaction identifiers, which show the funds being withdrawn or sent from their control to the fraudster. Following a traceable laundering process, funds can end up at centralised retail outfits like Binance, Kraken and Coinbase, offshore swapping services like SimpleSwap and ChangeNow, to purportedly decentralised outfits, who offer services without obtaining Know Your Client documents or Anti Money Laundering checks, performing permissionless transactions.

Once at these exchanges, victims need to know key information to consider the viability of pursuing a legal claim, including details of the exchange’s customer, information concerning internet-protocol addresses, trading histories and, of course, the balances held at accounts. Without this information, it is extremely difficult to consider whether a victim should spend good money chasing lost assets, and in most reported cases, victims have taken a high-risk approach in pursuing “persons unknown” with limited information.

To obtain this material, lawyers can use gateway 25(b) of the Civil Procedure Rules (which dictate the rules around litigation in England and Wales), which requires victims to start a substantive claim alongside an application for disclosure of information. This means they must be prepared to sue someone and detail the claim clearly at that stage.

As a commercial proposition, this might be extremely costly. The Law Commission recognises this at paragraph 3.78 of its report, where it states that “victims are not always able to say that they definitely intend to commence proceedings in England and Wales”

Similarly, to obtain wider reliefs against perpetrators, including a worldwide freezing injunction which prohibits the defendants from moving or dissipating their assets globally up to the value of the claim, the victim must also show from the outset that they have other assets to the value of the loss, on the basis that the injunction detriments the defendants unfairly. This is an enormous burden for any victim of fraud to overcome, without really knowing anything about the defendants.

Currently, the bar to entry is very high. Only those with deep pockets, and a high appetite for risk, can pursue their funds via the courts.

Should the proposal be successful, this would allow victims to assess the viability of the claim and consider the facts at hand without starting a formal claim. The costs might be substantially lower, and without the risk associated with formal litigation.

The proposed test for granting one of these orders is provided at paragraph 4.92 within the consultation paper, and summarised as:

The case has a certain strength, in that the claimant must evidence a wrongdoing;

The disclosure of this information is necessary to allow the victim to bring legal proceedings or other redress;

The court must be satisfied that there is no other court in which the claimant could reasonably bring the application for disclosure;

The court must be satisfied there is an adequate link to England and or Wales. For example, that the victim resides, domiciles or is a national here. This might also include (though not explicit in the paper) that the defendant purports to have an adequate connection to this jurisdiction – for example where a scam investment website says the company is registered in England.

Effect and next steps

In principle, this initiative will drastically lower the obstacles to recourse by giving victims a cost-effective solution to assess a claim’s viability and mitigate litigation risks early on. A consultation period for this paper is open until 8 September 2025, and many law firms and individuals have already backed the Law Commission’s above proposal, including both of us as authors of this piece as well as our peers including Nathan Capone at Fieldfisher.

This reform is vital in widening access to justice by revolutionising the initial stages of crypto asset recovery by removing substantial financial and procedural barriers that currently prevent many victims from commencing a claim.

To find out more about our Blockchain and Digital Assets services, please click here

Lawrence Stephens has partnered with Howden, the global insurance intermediary group, to launch a first-of-its-kind solution for the cryptocurrency sector. This innovative facility combines robust crypto theft insurance with expert legal asset recovery services, offering clients a comprehensive and credible response to digital asset theft.

The new solution delivers more than just insurance – it provides clients with a fully integrated approach that includes legal expertise, access to leading crypto vendors, and forensic recovery capabilities.

“At Howden, we believe in delivering solutions that go beyond traditional insurance,” said Freddie Palmer, Head of Digital Assets and Blockchain at Howden. “By partnering with Lawrence Stephens, we’re empowering our clients with a seamless, end-to-end service that combines technical insurance advice, legal recourse, and access to the broader crypto ecosystem. It’s a powerful response to one of the industry’s most urgent challenges.”

Key features of the facility include:

Specialist legal support from Lawrence Stephens to initiate asset freezing and recovery proceedings.

Insurance coverage that includes partial reimbursement of legal recovery costs when engaging Lawrence Stephens.

Access to a trusted network of crypto vendors and forensic experts to trace and recover stolen assets.

“We’re delighted to offer our legal expertise to the insurance market through this collaboration with Howden,” said Matt Green, Head of Blockchain, Digital Assets and Technology Disputes at Lawrence Stephens. “After all, the legal process began helping an insurer reclaim payment following a ransomware attack.”

This launch marks a significant step forward in institutionalising crypto asset protection, offering clients a credible, structured, and responsive solution in an increasingly complex digital landscape. As digital assets become more mainstream, institutional-grade protection is essential to build trust, reduce risk, and support the long-term growth of the crypto economy.

To find out more about our Blockchain, Digital Assets and Technology Disputes services, please click here

We now find ourselves at a critical crossroads in the evolution of financial technology. While the UK once made bold proclamations about becoming a global crypto asset hub, real progress has stalled, and the lack of regulatory clarity is beginning to weigh on investment, innovation, and job creation. In an era where blockchain, artificial intelligence, and quantum computing are converging to reshape global economies, the UK must act decisively or risk falling behind forward-thinking jurisdictions such as the US, Singapore, and the UAE.

While recent developments from the Financial Conduct Authority (FCA) – including the publication of a crypto roadmap and the UK Treasury preparing draft legislation to provide clarity on qualifying crypto assets, including stablecoins, which will fall under the remit of the Financial Services and Markets Act 2000 – indicate progress, the pace of change remains too slow.

The UK has a golden opportunity to define a forward-looking, globally competitive framework for digital assets, but this demands bold leadership, joined-up policymaking, and a clear national strategy that puts emerging technologies at the centre of economic growth. In a joint letter to government, Matt Green, Head of Blockchain and Digital Assets and Technology Disputes at Lawrence Stephens, together with leading industry bodies, outlined a series of proposals to help the UK realise this potential. The article below explores their key recommendations in more detail.

Laying the groundwork for growth

According to the FCA, around 12% of UK adults, approximately seven million people, now own digital assets. Despite this, only 8% of global venture capital funding in the space went to UK-based firms in the past year. The US, by comparison, attracted a staggering 76%. If the UK is serious about becoming a leading force in the digital economy, it must close this investment gap with urgency.

At present, a fragmented approach to digital asset regulation is inhibiting progress. A new wave of global strategies led by national governments eager to capture the economic benefits of blockchain and Web3 is leaving the UK at risk of playing catch-up. From Dubai to Washington, governments are launching clear action plans, appointing envoys, and rolling out incentive programs to attract high-potential digital firms.

A clear path to digital leadership

That’s why a coalition of leading trade bodies, including the UK Cryptoasset Business Council, Global Digital Finance, The Payments Association, techUK and Lawrence Stephens has come together to call on the Government to implement a clear digital asset strategy. Representing both pioneering start-ups and established multinational firms, we believe the UK can and should be at the forefront of responsible innovation.

There are four key steps the UK can take to realise this ambition:

1. Appoint a blockchain special envoy

Just as the US government has appointed a high-profile blockchain envoy to spearhead policy alignment and investment attraction, so too must the UK. A dedicated envoy would serve as a strategic bridge between government, regulators, and industry, driving consistency, championing innovation, and positioning the UK as a premier destination for blockchain-related investment. The envoy would also play a crucial global role, representing the UK on the international stage and securing collaboration opportunities with leading digital nations.

2. Launch a government-led Digital Asset Action Plan

Like the coordinated approach seen in artificial intelligence, the UK should implement a comprehensive strategy for digital assets and blockchain technology. This could include a white-glove concierge service to support scale-ups, integration of blockchain into public services, and the development of a globally competitive tax and investment landscape. Targeted incentives would enable the UK to attract and retain the world’s most promising digital firms, ensuring job creation and long-term economic benefit.

3. Recognise the convergence of emerging technologies

Emerging technologies rarely operate in silos. Blockchain, quantum computing, and AI are increasingly interdependent, and together they promise to redefine industries from finance and defence to supply chains and public healthcare. For example, blockchain can add transparency and trust to AI systems, while AI can optimise blockchain functionality. These technologies working in harmony offer the potential to deliver transformative public services, from decentralised property registries to secure NHS data transfers. The UK must actively foster collaboration across these disciplines to maximise impact and support innovation at scale.

4. Create an industry-government engagement forum

Effective policymaking must be informed by those at the forefront of innovation. To that end, we propose the creation of a high-level industry-government-regulator taskforce, designed to ensure close collaboration and continuous dialogue across sectors. This would enable agile policymaking that reflects the rapidly evolving nature of digital technologies and ensures the UK remains ahead of the curve.

Unlocking long-term economic value

The potential economic impact of digital assets and blockchain is immense. A recent PwC report projects that blockchain could add £57 billion to the UK economy over the next decade. Globally, it could boost GDP by £1.39 trillion by 2030. Sectors like logistics, finance, health, and public services stand to gain the most, particularly through improved transparency, faster data transfers, and streamlined transactions.

Meanwhile, the UK’s legal infrastructure is increasingly ready to support these developments. The Law Commission’s recent endorsement of a new ‘third category’ of property to account for digital assets is a significant step forward, strengthening the legal foundation for cryptoassets, tokenised securities, and carbon credits. In doing so, the UK is proving it has both the legal and technological credibility to lead on digital assets.

Now is the time to act

The UK’s digital asset economy is already the largest in Europe, with £172 billion in on-chain transactions last year. Yet without bold, strategic intervention, we risk being eclipsed by more proactive nations. As innovation accelerates and geopolitical dynamics shift, the UK must seize its moment.

With the right leadership, a coherent regulatory environment, and an ambitious vision for innovation, we believe the UK can cement its status as a global hub for digital assets and blockchain technology.

Now is the time to move from ambition to action.

If you have queries on the above, please contact Matt Green.

Director and Head of Blockchain and Digital Assets, Matt Green, comments on the recent series of attempted kidnappings of crypto entrepreneurs and discusses how to best protect assets stored on the blockchain, in The Next Web.

Matt’s comments were published in The Next Web, 29 May 2025, and can be found here.

“Despite the industry pining for decentralisation, much of the data points towards identifiable individuals with either massive wealth or access to third parties’ wealth. Simple blockchain analytics openly identifies addresses holding fortunes, and once those addresses are associated with named individuals (data triaging and clustering can unmask a pseudonymised address), then criminals can see very clearly that a person holds significant wealth. Imagine your bank balances are posted online and through analysing open source data, the world can see it’s your account.

“In terms of crypto holders, the only thing stopping criminals gaining access is human error or force so kidnapping aims to break down the integrity of that human led security.

“The nature of blockchains means balances and addresses are public. In the same way van stickers read “no tools are kept in this vehicle”, it might be worth making a conscious effort to show a single person under duress is incapable of giving access to crypto holdings. Having clear statements about Multi-Sigs (Multi-Signature wallets) would likely deter kidnappers, who would have to pursue multiple individuals to make gains.”

To out more about our work on blockchain, crypto and digital assets, please click here